We all are particularly concerned about our children’s future and the cost of education. As parents, it is completely normal to be worried. In current times, parents of a child reading in Nursery are already burdened with huge fees and other educational expenses. Such huge expenses in pre-primary classes were unthinkable in the past. Families followed the Traditional Approach where after the birth of a child, a Child Insurance Plan was purchased from a known LIC agent or the grandparents of the child gave money to be deposited under some Child Scheme in a bank or other investment instruments.

In the case of this Traditional Approach, how much expenses would be incurred in the future was not known nor calculated. It is because of two reasons- inflation wasn’t so high and banks, post offices offered good interest rates. Presently, the economical situation of our country has drastically changed. You may say that you don’t understand such complex terms. I will tell you need not understand and I am not here to discuss them either. Now think about your salary that you received for your post 15 years ago. Are you still on the same salary package? Definitely not, so why has your salary increased? Do find out about the monthly expenses your father had spent on household items. Are you spending the same amount? Definitely not. Why has it increased? The general increase in prices of various commodities is one of the many reasons for our daily expenses to rise. This is called Inflation.

Moreover, you can ask your father or uncle how they ran their households, solely on the interest rates that were provided by banks and post offices. This scenario is no longer seen in the present times, isn’t it? Earlier, one could get enough money to run a family from the interest given by banks and post offices but the scenario has changed now. The interest rates have fallen drastically even if the sum of money is huge. Earlier the inflation rate was low but the interest rates were higher.

The question now arises, why such an increase? There are various reasons for it which I have stated earlier. The sad part is that people are ignoring the present and still holding onto the Traditional Approach. The consequences can be terrible. The parents who think the Child Insurance Policy can bear all the future education costs of their son/daughter then they are very wrong. Don’t take me in the wrong sense, just think about how the cost of education and health services is inflated every year. The basic thing one should know is that in order to fight against Inflation and get a higher return, one needs to invest in creating the right Provision to avail the Compounding Effect. The Main Return in Insurance is a Bonus that cannot be compounded. An earlier article in this blog will tell you the nature of interest rates and inflation in our country in the last 35 years. If you haven’t read it yet, click here.

I am sharing a practical incident here. One of my clients, Salil babu (named change) who was referred by another of our clients, came to our office in the year 2000. He was worried and wanted to discuss his child’s Education Planning and informed us that he had purchased a 3 lacs sum assured Child Insurance Plan. He was paying 24, 332 every year as a premium. When he purchased the policy, the child was 3 years old.

Those days even I did not have much idea about Goal Planning. However, I knew the effects of Inflation and how it worked so I advised him to set a Target amount otherwise he wouldn’t reach his goal. We discussed and came to a conclusion that the target amount be set to 8,50,000. Nevertheless, he believed that the amount wasn’t enough to fulfill his purpose so I suggested him to start a SIP with 2000 rupees each month.

His child was 4 then. I explained to him that in 14 years, if he continues to deposit 2000, then it wouldn’t be difficult to reach his goal.

Due to his lack of knowledge about Mutual Funds, a lot of discussions and convincing made him change his mind. He decided to invest in SIP for 5 years as for now then he’d decide if he would continue or not.

Today the fund is on the way to maturity. More importantly, Salil babu who once did not want to continue his investment for more than 5 years has a SIP of Rs. 38,000 now. His son is of 18 years now and has appeared for his boards in the year 2015. A few days back, we sat together for an Investment Review.

This year Salil babu has already received a sum of 75,000 from the Insurance policy. Also, he would be receiving 75,000 rupees when his son turns 19, 20, and 21. Also, when the policy matures, he would be receiving a sum of 1,80,000 rupees. Which means he invested 24,332 for 18 years i.e 24,332×18= 4,37,976 rupees and he received 75,000×4=3,000,00+1,80,000= 4,80,000 rupees.

The Mutual Fund in which he was investing 2000 rupees each month, the value of that fund is 18,17,252. Salil babu has invested 2000 rupees in this fund for 14 years which has amounted to 3,36,000 rupees. This amount is a lot more than his target amount.

Someone can say that the particular Insurance Policy had coverage of 3 lac rupees which is correct. However, Salil babu’s purpose was different. He wanted Provision for Education for his son’s education. If he would have wanted Life coverage, he would have opted to invest 48,000 a year for his son’s Educational Planning Provision; estimating the monthly income, he would be needing a lot more coverage, isn’t it?

Some people may say that his income was good so he could invest in Mutual Funds and risk his money. There are certain types of risks which are called Perceive risks. Perceive risks are those which are perceived in the minds of an individual. These risks are unlikely to happen. It is important to determine the reality and myth factor in risk. Risk is not always loss. Risk= Previous Experience is also incorrect. Risk=Myth or Risk=Some Unknown Thing is also incorrect.

My suggestion is to take small steps if one is a little apprehensive about taking risks. You can start with a small investment and then later decide whether to take the next step. For example, if a baby starts running just after he is born, that would be highly risky for him. Therefore, he starts by crawling, then requires support and finally walks on his own. This is the rule. The important part is you need to take a small step first.

There are scientific techniques to manage risk in finance. But if someone believes that everything is risky, I’d request them to think clearly and start investing with a small amount. Can you say how the dish tastes unless you consume it? Similarly, unless you try you wouldn’t be able to overcome any sort of fear.

Please do not assume that the return was made for the Fund in which Salil Babu invested in. It is a wrong assumption. The Equity Market has fluctuated innumerable times between the years 2000 to 2015. During those years, Salil babu had never thought of applying for a Profit Book nor stopped paying for his SIP. At times, he did face many such situations which could make him think otherwise but instead, we sat down, discussed in detail about his situations and his faith and trust increased.

Salil Babu ( named changed) is a regular reader of our blog. Forgive me, Salil Babu. But I know, no one will be happier than you if you come to know that someone has benefited from your example.

Many of you have sent questions that I am trying to answer here.

Q. What is the best investment for a child?

A: I think the question will be where should one invest for their child’s Higher Education.

I don’t know if there is any such Fund in India where all your financial problems could be solved. What you need is proper Financial Planning to get rid of such difficulties in the future. You need to know after how many years would you be needing money for your child’s Higher Education. You also need to determine the course that he would take up and most importantly the educational inflation rate. Basically, one has to find out his future expenses i.e the Target Amount.

If you are planning to invest for the next 7 years then you may choose any Diversified Fund of Equity Mutual Fund. But only Planning would not help, one needs to Review the plan from Time to Time.

Q: Where can I invest money for my child’s education?

A: Answer given in the previous question.

Q: Which is the best plan for child education?

A: There is nothing called the best plan. A plan is a plan. I think the correct question should be which is the best fund for child education. Unfortunately, I have no idea which is the best fund. If someone knew which fund would have the highest returns then that someone would not let anyone know and become the richest person on earth.

You may invest in any Diversified Fund of Equity Mutual Fund for a Long time Investment or you may invest in a Large Cap Fund where the Returns are higher and they can beat Inflation too.

No matter which fund you invest in, you need to see whether it can beat inflation and has good returns. The Performance of the Fund has to be Periodically Reviewed.

Q: How do you plan for your child’s education?

A: I am listing down a few steps so that you may plan for your child’s Education Planning on your own.

Step 1. You need to find out the time or years left for your child to pursue higher education.

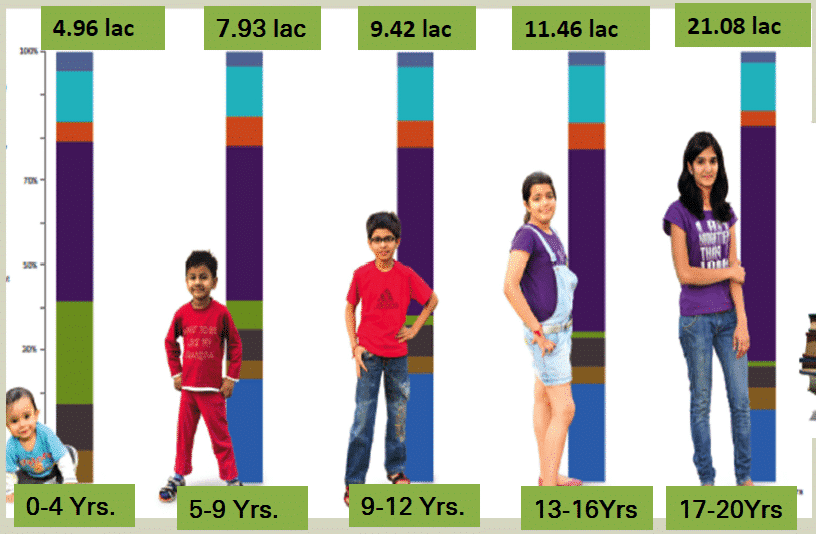

Step 2. You need to know which course your child wants to pursue. Then you need to find out the course fees at present. These two factors are the most important to determine the cost of Education Planning. Now to find out the Future Cost, you need to know about the inflation rate. Suppose the inflation rate is at 9% and the present Education Cost is 10,000,00 then after 15 years, the cost of the same course will be 36.42 lacs. Similarly, if the inflation rate is 10% or 12%, then the cost will be 54.73 lacs.

A Recent Study Report showed the various courses available to pursue and their course fees. The list is below-

- Medical Rs 64 Lakh in 4 Yrs

- Medical Oversees Rs 90 Lakh

- Engineering Rs 9 Lakh

- Engineering in Overseas Rs 40 Lakh

- MBA in India 24 Lakh

- MBA in Overseas 64.76 Lakh

- Law in India 2.5 Lakh

- Law Overseas 50 Lakh

- Architecture in India 4 lakh

- Architecture Overseas 4 Lakh

- Hotel Management in India 3.5

- Hotel Management in overseas 45 Lakh

Step 3: Existing Investment regarding this Goal

If any earlier investment is done regarding this goal, it needs to be considered too.

Step 4: Investment Now Required?

After considering these steps, you will get an idea of how much investment is required. If someone is unable to invest a one-time lump sum amount, he can go for monthly investments too.

Step 5: Review Plan Periodically

Once the Planning is done, you have to see if the plan is working in real or if the fund is performing well.

Step 6: Take Adequate Insurance Coverage

It is important to have an adequate amount of Term Insurance for the main earner of the family on whose income this Education Planning depends.

Step 7: Preparing an Emergency Fund

No matter how you plan, no matter what you plan for, everything may not happen the way you have planned. So it is necessary to create an emergency fund for any adversity in the future.

Q: How do you plan your child’s future?

A: I guess I have been successful in answering this question. Please read the article above.

Note: The examples or return % used are just to explain the concept of SIP. Mutual Funds are subjected to Market risk, kindly read the offer document before investing.

I am just an AMFI Certified Mutual Fund Distributor and this article has no purpose of planning or advising anyone but to clear the concept of SIP and create awareness for the same.

If you want to add some value to this article, feel free to write to us. Your feedback is important to us.